新用戶掃碼下載

新用戶掃碼下載

掃碼下載APP

及時接收考試資訊及

備考信息

PRINCIPLES UNDERPINNING MEASUREMENT OF REVENUE

IAS 18 states that ‘Revenue shall be measured at the fair value of the consideration received or receivable’ (12). In determining fair value it would be necessary to take into account any trade discounts or volume rebates granted by the seller.

In most cases, ‘fair value’ will represent the cash or cash equivalents received or receivable by the seller. However, where the consideration is deferred, IAS 18 explains that the arrangement effectively constitutes a financing transaction and the substance of the transaction is a supply of goods or services plus the provision of finance. In such circumstances, the amount receivable is split into (13):

(a) An amount receivable for the supply of goods or services. This is arrived at by discounting the future cash receivable by the seller. The imputed rate of interest is the prevailing borrowing rate of the buyer or, if more easily determinable, the rate that discounts the future cash receivable to the current cash price of the goods or services. This is recognised immediately.

(b) An amount receivable for the supply of finance to the buyer, recognised over the implied term.

Example

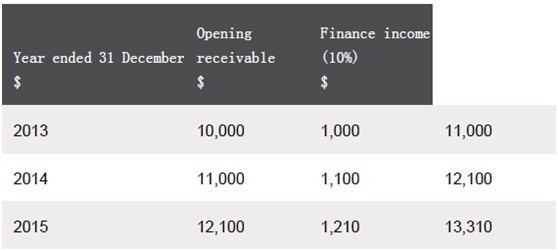

A retail entity supplies products to the public on three year deferred payment terms. On 1 January 2013 the entity supplies a product for a total price of $13,310, payable on 1 January 2016. The credit rating of the customer is such that a relevant imputed annual rate of interest is 10%. The entity’s year end is 31 December.

On 1 January 2013 the total revenue from the sale would be split into:

(a) Revenue from the sale of goods of $10,000 ($13,310/(1.10) (3). This is recognised immediately by crediting revenue and debiting receivables.

(b) Interest revenue of $3,310 ($13,310 - $10,000). This is recognised over the three years as shown in the table below:

On 1 January 2016, the cash is received and the receivable derecognised.

IAS 11 uses similar principles to measure revenue from construction contracts, stating that ‘Contract revenue is measured at the fair value of the consideration received or receivable’ (14).

IAS 18 IMPLEMENTATION EXAMPLES

As stated earlier, these implementation examples accompany, but are not part of, IAS 18. However they are useful as an aid to application and well worth reviewing. They assume that the amounts of revenue and related costs can be measured reliably, and that the economic benefits will probably flow to the seller. Most of the examples are relatively self-explanatory. We will review two of the more complex examples:

Example 5 – sale and repurchase agreements (15)

Where goods are ‘sold’ under conditions that either require the seller to repurchase them in the future or contain options to repurchase that are likely to be exercised then the substance of the transaction of often that the ‘sale’ is actually a provision of finance.

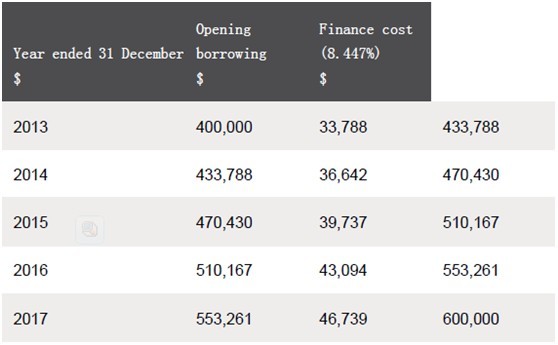

Suppose entity A ‘sells’ goods to entity B on 1 January 2013 for $400,000. The goods are inventories that need to mature for five years before being ready for sale. Their market value on 1 January 2013 was $800,000 and entity A has the option to repurchase the goods from entity B on 1 January 2018 for $600,000. The market value of the goods is expected to rise by 5% per annum from 2013 to 2017 inclusive. Entity A’s credit rating is such that it would have to pay interest at 8.447% per annum on borrowings. The goods are expected to remain at the premises of entity A throughout the five year period beginning on 1 January 2013 and entity A is responsible for their safe custody.

The fact pattern in this example indicates that at least two of the conditions required for the recognition of revenue on the sale of goods have not been satisfied:

· Entity A retains the risks and rewards of ownership despite the fact that legal ownership has been transferred to entity B.

· Entity A retains managerial involvement to the degree usually associated with ownership.

Therefore it is inappropriate for entity A to recognise revenue when the goods are sold on 1 January 2013. The ‘sales proceeds’ should be recognised as a borrowing with an annual finance cost of 8.447%. Over the next five years the borrowing will grow as follows:

The almost certain ‘re-purchase’ on 1 January 2013 will eliminate the borrowing.

Example 11 – servicing fees included in the price of a product (15)

When the selling price of a product includes an identifiable amount for subsequent servicing that amount is deferred and recognised as revenue over the period during which the service is performed. The amount deferred is that which will cover the expected costs of the services, together with a reasonable profit on those services.

Suppose an entity supplies a product to a customer for a total price of $20,000. The price includes two years ‘free’ servicing of the product. The entity estimates that the annual cost of servicing the product will be $2,400. The entity normally earns a margin of 20% on service revenue.

The expected total cost to the entity of providing the ‘free service’ is $4,800 (2 X $2,400). Given the normal margin on service work this would equate to revenue of $6,000 ($4,800 X 100/80). Therefore the entity would recognise revenue from the sale of the product of $14,000 ($20,000 - $6,000) at the date of supply and service revenue of $6,000 over the two years following the supply.

The situation is further complicated when a ‘package’ such as the one outlined above is supplied at a special price and the fair value of both components is known. Suppose in the above example the normal selling price of the product without any

‘free’ servicing was $18,000. We would then have two components to the transaction with fair values totalling $24,000 ($18,000 for the product + $6,000 for the servicing). If the whole package were supplied for $20,000 then this would be at 20/24 or 5/6 of the ‘normal’ price. This would be allocated to the components so that the total revenue of $20,000 would be allocated as follows:

· Sale of goods $15,000 ($18,000 X 5/6).

· Service revenue $5,000 ($6,000 X 5/6).

CHANGES THAT ARE LIKELY TO THE METHOD ACCOUNTING FOR REVENUE IN THE FUTURE

The background

As already stated, revenue is a crucial number to users of financial statements in assessing an entity’s financial performance and position. However, revenue recognition requirements in US generally accepted accounting principles (GAAP) differ from those in International Financial Reporting Standards (IFRSs).

Both sets of requirements need improvement. US GAAP comprises broad revenue recognition concepts and numerous requirements for particular industries or transactions that can result in different accounting for economically similar transactions. Although IFRSs have fewer requirements on revenue recognition, the two main revenue recognition standards, IAS 18, Revenue and IAS 11, Construction Contracts, can be difficult to understand and apply. In addition, IAS 18 provides limited guidance on important topics such as revenue recognition for multiple-element arrangements.

The detail

The International Accounting Standards Board (IASB) and the US national standard-setter, the Financial Accounting Standards Board (FASB), initiated a joint project to clarify the principles for recognising revenue and to develop a common revenue standard for IFRSs and US GAAP that would (16):

(a) Remove inconsistencies and weaknesses in existing revenue requirements

(b) Provide a more robust framework for addressing revenue issues

(c) Improve comparability of revenue recognition practices across entities, industries, jurisdictions and capital markets

(d) Provide more useful information to users of financial statements through improved disclosure requirements, and

(e) Simplify the preparation of financial statements by reducing the number of requirements to which an entity must refer

The proposed requirements would affect any entity that enters into contracts with customers unless those contracts are in the scope of other standards (for example, insurance contracts or lease contracts).

To achieve that core principle, an entity would apply all of the following steps (17):

(a) Identify the contract with a customer.

(b) Identify the separate performance obligations in the contract.

(c) Determine the transaction price.

(d) Allocate the transaction price to the separate performance obligations in the contract.

(e) Recognise revenue when (or as) the entity satisfies a performance obligation.

From an IFRS perspective, the new standard arising out of the project is likely to be more robust than the existing standards. This should assist in future convergence between IFRS and US GAAP.

The project is in its final stage of development and a new standard is likely to apply for accounting periods beginning on or after 1 January 2017.

References

1. Paragraph 7 – IAS 18.

2. Paragraph 14 – IAS 18.

3. Paragraph 20 – IAS 18.

4. Paragraph 24 – IAS 18.

5. Paragraph 26 – IAS 18.

6. Paragraph 3 – IAS 11.

7. Paragraph 22 – IAS 11.

8. Paragraph 23 – IAS 11.

9. Paragraph 30 – IAS 11.

10. Paragraph 32 – IAS 11.

11. Paragraph 29 – IAS 18.

12. Paragraph 9 – IAS 18.

13. Paragraph 11 – IAS 18.

14. Paragraph 12 – IAS 11.

15. IAS 18 IE

16. IN 2, ED 2011/6 Revenue from Contracts with Customers

17. Paragraph 4, ED 2011/6 Revenue from Contracts with Customers

Previous>> See the original article>>

Copyright © 2000 - www.electedteal.com All Rights Reserved. 北京正保會計科技有限公司 版權所有

京B2-20200959 京ICP備20012371號-7 出版物經營許可證 ![]() 京公網安備 11010802044457號

京公網安備 11010802044457號

套餐D大額券

¥

去使用 主站蜘蛛池模板: 国产一区久久久 | 国产三区四区 | 精品久久一区二区三区 | 国产精品美女久久久久久久网站 | 亚洲精品一区二区三区在线 | 色中文字幕在线观看 | 久久999免费视频 | 亚洲一区二区黄色 | 亚洲国产日韩精品 | 国产欧美日韩综合精品 | 国产一区二区三区在线看 | 九色最新网址 | 国产日韩亚洲 | 亚洲综合在线视频 | 国产精品久久久久久久久久 | 国产剧情在线观看一区 | 欧美天堂一区 | 偷拍视频一区二区 | 精品九九久久 | 日韩高清在线观看 | 午夜精品 | 国产精品一级片 | 日韩视频免费在线观看 | 国产黄色免费网站 | 亚洲国产日韩精品 | 久久精品视频一区二区三区 | 国产高清不卡av | www.色五月.com| 在线观看黄色一级片 | 偷拍自拍亚洲色图 | 国产一区二区三区精品久久久 | 男人都懂的网站 | 偷拍第一页 | 999毛片 | 999久久久久久久久6666 | 一区二区三区中文字幕 | 精品一区二区三区四区 | 日本成人在线播放 | 色伊人| 最新日韩精品 | 国产一区二区在线观看视频 |

新用戶掃碼下載

新用戶掃碼下載