掃碼下載APP

及時(shí)接收考試資訊及

備考信息

新用戶掃碼下載

新用戶掃碼下載安卓版本:8.7.95 蘋果版本:8.7.95

開發(fā)者:北京正保會(huì)計(jì)科技有限公司

應(yīng)用涉及權(quán)限:查看權(quán)限>

APP隱私政策:查看政策>

HD版本上線:點(diǎn)擊下載>

ACCA官網(wǎng)已公布2016年ACCA試題,網(wǎng)校特別為大家整理以下試題,希望能夠幫助您查漏補(bǔ)缺、鞏固知識(shí)點(diǎn),在考場(chǎng)上發(fā)揮自如。

網(wǎng)校為廣大ACCA學(xué)生提供免考科目預(yù)評(píng)估服務(wù),您可以點(diǎn)擊![]() 按鈕進(jìn)行評(píng)估申請(qǐng)。

按鈕進(jìn)行評(píng)估申請(qǐng)。

Question:

(a)GFH Ltd,a manufacturing company set up in Xi'an,produces and sells integrated circuits to an overseas associated company. It has not applied for the tax incentives for integrated circuits enterprises. GFH Ltd's statement of profit or loss for the year ended 31 December 2015 is as follows:

The following information is relevant to the items charged/credited in the above statement of profit or loss:

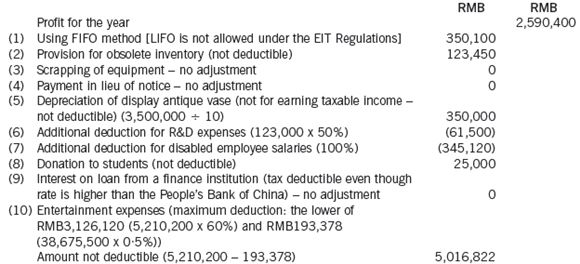

(1)The accountant has used the last in,first out (LIFO)method to value the inventories. If the first in,first out(FIFO)method were used,the cost of goods sold would have been reduced by RMB350,100.

(2)The increase in the provision for obsolete inventory was RMB123,450.

(3)A piece of equipment with a net book value of RMB80,000 was scrapped for nil proceeds.

(4)RMB1,000,000 was paid to a senior production manager in lieu of notice for early dismissal.

(5)In 2014,an antique vase was bought for RMB3,500,000 and put in the CEO's room for display. A ten-year economic life without scrap value has been used to calculate depreciation on this asset.

(6)Research and development expenses of RMB123,000 were incurred for a project which qualifies for an additional tax deduction.

(7)The salaries of the disabled employees hired by GFH Ltd in 2015 were RMB345,120. This cost qualified for the tax incentive.

(8)A donation of RMB25,000 was made to some students of a remote school.

(9)Interest at the rate of 25% per annum was paid on a loan of RMB8,000,000 from a finance institution in Xi'an. The interest rate of the People's Bank of China was 5%.

(10)Entertainment expenses incurred were RMB5,210,200.

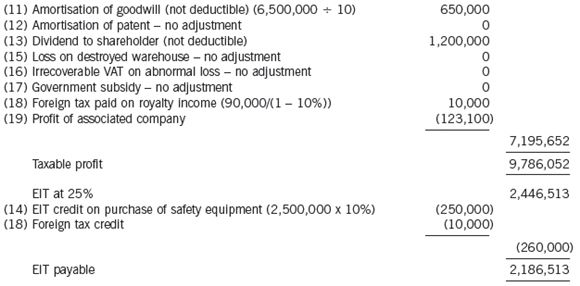

(11)GFH Ltd acquired a new business in 2013 and paid RMB6,500,000 for the business' goodwill. This goodwill is being amortised over a period of ten years.

(12)GFH Ltd acquired a patent from another company in 2014 and paid a fee of RMB3,200,000. This patent fee is being amortised over a period of ten years.

(13)The dividend payable to the shareholder of GFH Ltd of RMB1,200,000 was treated as part of costs and expenses.

(14)Newly acquired equipment costing RMB2,500,000 qualifies under the Safety Production Special Equipment Catalogue.

(15)A warehouse was destroyed by a flood. The loss incurred of RMB150,000 was not covered by insurance.

(16)Irrecoverable input value added tax (VAT)on an abnormal loss amounted to RMB119,000.

(17)A subsidy of RMB3,000,000 was received from the Xi'an government for a specific project in 2013. The project was completed in 2015 and the amount spent on the project totalled RMB2,789,500. The balance of RMB210,500 was treated as income of 2015.

(18)GFH Ltd has granted an associated company in Vietnam the right to use its technology. The royalty income received of RMB90,000 was after the deduction of 10% Vietnamese withholding tax.

(19)GFH Ltd invested in an associated company in India in 2010. The profit of RMB123,100 is the proportion of the associate company's profit attributable to GFH Ltd and is included in its consolidated accounts. GFH Ltd pays enterprise income tax (EIT)at the standard rate.

Required:

Calculate the enterprise income tax (EIT)payable by GFH Ltd for the year 2015,assuming that GFH Ltd has made all the relevant applications.

Note: You should start your computation with the net profit figure of RMB2,590,400 and list all of the items referred to in notes (1)to (19)identifying any items which do not require adjustment by the use of zero (0).

(b)The company's accountant has proposed that GFH Ltd should apply for the following enterprise income tax (EIT)

incentives for the year 2015:

(1)a qualified integrated circuit enterprise; and

(2)an encouraged industry under the Central and Western catalogue.

Required:

State the preferential treatments available under each of these two enterprise income tax (EIT)incentives.

Answer:

GFH Ltd

(a)Enterprise income tax (EIT)for 2015

(b)Preferential treatments available

(1)Qualified integrated circuit enterprise: a two-year exemption and three-year half rate of EIT starting from the first profit making year.

(2)Encouraged industry under the Central and Western catalogue: 15% tax rate until the end of 2020.

掃一掃關(guān)注更多ACCA考試資訊

歷年樣卷

考試大綱

詞匯表

報(bào)考指南

考官文章

思維導(dǎo)圖

新用戶掃碼下載

新用戶掃碼下載安卓版本:8.7.95 蘋果版本:8.7.95

開發(fā)者:北京正保會(huì)計(jì)科技有限公司

應(yīng)用涉及權(quán)限:查看權(quán)限>

APP隱私政策:查看政策>

HD版本上線:點(diǎn)擊下載>

官方公眾號(hào)

微信掃一掃

官方視頻號(hào)

微信掃一掃

官方抖音號(hào)

抖音掃一掃

Copyright © 2000 - www.electedteal.com All Rights Reserved. 北京正保會(huì)計(jì)科技有限公司 版權(quán)所有

京B2-20200959 京ICP備20012371號(hào)-7 出版物經(jīng)營許可證 ![]() 京公網(wǎng)安備 11010802044457號(hào)

京公網(wǎng)安備 11010802044457號(hào)

套餐D大額券

¥

去使用 主站蜘蛛池模板: 国产二区免费视频 | 91精品国产综合久久小美女 | 成人免费视频在线观看 | 亚洲成人99 | 尤物网站在线 | 国产欧美一区二区三区在线看 | 日韩 国产 在线 | av电影网址在线观看 | 久久有精品 | 久久久综合激的五月天 | 国产999精品久久久久久 | 精品一区二区免费视频 | 国产二区免费 | 国产免费视频在线 | 日本一区二区三区在线观看视频 | 国产福利资源 | 精品电影一区二区三区 | av中文在线资源 | 国产精品美女www | 日韩欧美在线一区二区 | 国产美女视频一区 | 免费91视频 | 久久综合中文 | 日韩在线观看中文字幕 | 久久国产精品99久久久大便 | 国产成人精品综合 | 国产一区91在线 | 男女免费网站 | 国产a免费| 超碰成人91| 性色av一区二区 | 国产精品一二三区 | 99久久久无码国产精品 | 一本一本久久a久久精品牛牛影视 | 久久av二区| 国产高清免费 | 精品久久久久久久久久 | 日韩激情视频 | 日韩午夜在线 | 九九资源站| 亚洲色图在线观看 |