新用戶掃碼下載

新用戶掃碼下載

掃碼下載APP

及時接收考試資訊及

備考信息

Rates of tax

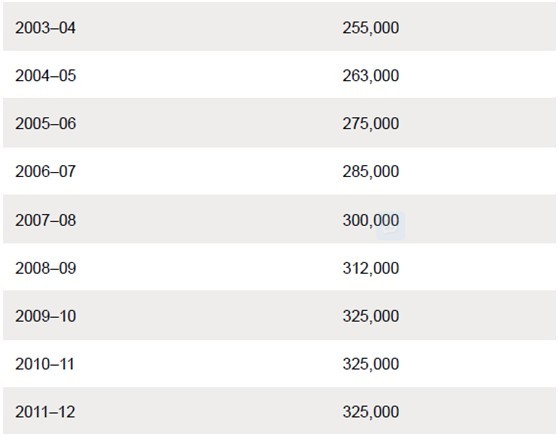

IHT is payable once a person’s cumulative chargeable transfers over a seven-year period exceed a nil rate band. For the tax year 2012–13 the nil rate band is £325,000, and for previous years it has been as follows:

The rate of IHT payable as a result of a person’s death is 40%. This is the rate that is charged on a person’s estate at death, on PETs that become chargeable as a result of death within seven years, and is also the rate used to see if any additional tax is payable on CLTs made within seven years of death.

The rate of IHT payable on CLTs at the time they are made is 20% (half the death rate). This is the lifetime rate.

The tax rates information that will be given in the tax rates and allowances section of the June and December 2013 exam papers is as follows:

Where nil rate bands are required for previous years then these will be given to you within the question.

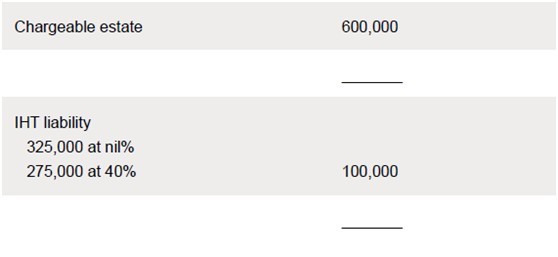

Example 4

Sophie died on 26 May 2012 leaving an estate valued at £600,000.

The IHT liability is as follows:

Death estate

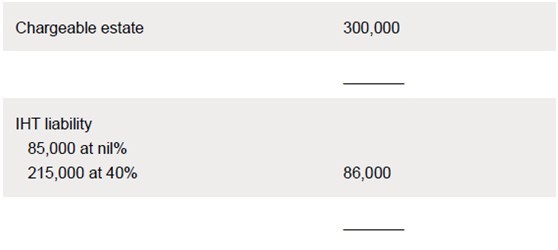

Example 5

Ming died on 22 April 2012 leaving an estate valued at £300,000.

On 30 April 2010 she had made a gift of £240,000 to her son. This figure is after deducting available exemptions.

IHT liabilities are as follows:

Lifetime transfer – 30 April 2010

· Only £85,000 (325,000 – 240,000) of the nil rate band is available against the death estate.

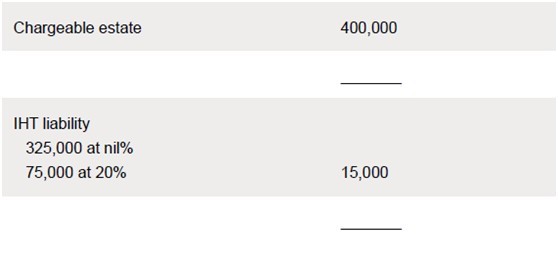

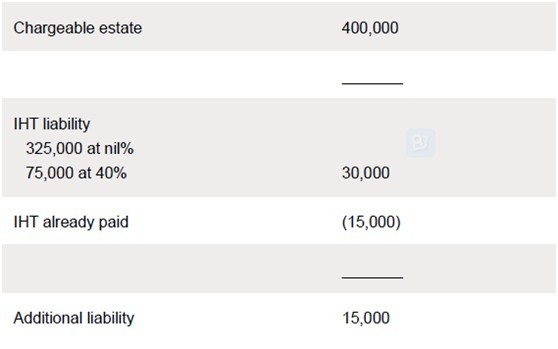

Example 6

Joe died on 13 October 2012 leaving an estate valued at £750,000.

On 12 November 2009 he had made a gift of £400,000 to a trust. This figure is after deducting available exemptions. The trust paid the IHT arising from the gift.

The nil rate band for the tax year 2009–10 is £325,000.

Lifetime transfer – 12 November 2009

· The gift to a trust is a CLT. The lifetime IHT liability is calculated using the nil rate band for 2009–10.

Additional liability arising on death – 12 November 2009

· The additional liability arising on death is calculated using the nil rate band for 2012–13.

Death estate

· The CLT made on 12 November 2008 has fully utilised the nil rate band of £325,000.

Page:1 2 See the original>>

Copyright © 2000 - www.electedteal.com All Rights Reserved. 北京正保會計科技有限公司 版權所有

京B2-20200959 京ICP備20012371號-7 出版物經營許可證 ![]() 京公網安備 11010802044457號

京公網安備 11010802044457號

套餐D大額券

¥

去使用 主站蜘蛛池模板: 国产三级电影在线观看 | 亚洲国产精品一区二区第一页 | 色先锋影院| 国产一区二区三区在线免费观看 | 免费看羞羞的视频 | av亚洲在线 | 日韩在线色 | 久久国产午夜 | 日日夜夜天天综合 | 国产精品网址 | 国产成人av在线 | 动漫av一区 | 成人在线一区二区 | 久久久综合精品 | 亚洲午夜久久久久 | 国产精品99久久久久久似苏梦涵 | 欧美一区二区三区在线看 | 精品久久国产 | 久久久久久一区二区三区四区别墅 | av免费观看网站 | 精品久久久一区 | 亚洲第一免费播放区 | 在线小视频 | 男人视频网站 | 欧美一区二区三区在线观看 | 欧美在线不卡视频 | 成人在线视频免费 | 欧美亚洲免费 | 性一区| 久久综合成人精品亚洲另类欧美 | 国产成人精品综合 | 成人av专区 | 男女69| 五月色综合 | 欧美天堂在线 | 久热福利视频 | 久久综合九色综合网站 | 国产婷婷色一区二区三区 | 国产婷婷综合网 | 久久久久久国裸歌舞团 | 成人国产精品久久久 |

新用戶掃碼下載

新用戶掃碼下載