新用戶掃碼下載

新用戶掃碼下載

掃碼下載APP

及時接收考試資訊及

備考信息

EXAMPLE 1

ABC Partnership

Table 1 shows the appropriation account for the year ended 31 December 2005. In an exam, the examiner might include the partners’ salary as wages and salaries in the income statement/profit and loss account. This would mean that the net profit would need adjusting, which would involve adding the partners’ salary to the net profit given in the question.

EXAMPLE 2

ABC Partnership

Table 2 shows the current account as at 31 December 2005.

EXAMPLE 3

ABC Partnership

Table 3 shows the capital account as at 31 December 2005.

EXAMPLE 4

Here is an illustrated example of the workings of a partnership business, and the treatment of goodwill on the admission of a new partner.

Jess and Tash are in partnership and share profits and losses in the ratio of 6:4 respectively. Jess is allowed an annual salary of $28,000 and Tash is allowed an annual salary of $25,000. The partners prepare their accounts annually at 31 December. The balances on the partners’ current and capital accounts at 1 January 2005 are as follows:

Due to the expansion and success of the business, the partners admitted Sash into the partnership on 1 April 2005. Sash introduced $500,000 as capital. On that date, the partners valued the goodwill as $200,000. After the admission of Sash, the partnership arrangements are as follows:

Profit and losses will be shared as follows:

– Jess: 50%

– Tash: 30%

– Sash: 20%

Partners will be credited with 5% of the interest on their capital balance at the start of the year

Interest on drawings will be charged at 8% per annum

The partners’ drawings during the year are as follows:

– Jess: $40,000 to 31 March and $60,000 to 31 December

– Tash: $30,000 to 31 March and $50,000 to 31 December

– Sash: $50,000 to 31 December

Sash will be allowed an annual salary of $20,000. Jess and Tash will continue to receive their annual salary

The goodwill must be eliminated from the records

During the year ended 31 December 2005, the partnership reported a profit of $526,000 after writing off a bad debt of $6,000 on 31 March 2006

The partners’ annual salary was deducted as an expense in the income statement/profit and loss account under wages and salaries.

Requirement

Prepare the following:

(a) Partners’ capital accounts as at 31 March 2005

(b) Partners’ appropriation account for the year ended 31 December 2005

(c) Partners’ current accounts as at 31 December 2005

(d) Balance sheet extract (Capital) as at 31 December 2005.

Answer

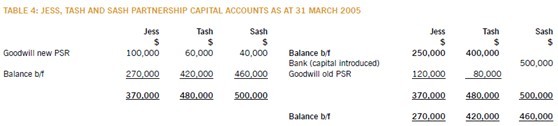

(a) Jess, Tash and Sash Partnership

Table 4 on page 65 shows the capital account as at 31 March 2005.

Goodwill is the excess market value of the business over its book value. It is only fair that the partners who created this goodwill – Jess and Tash

– should benefit from it, due to the hard work they have put into the business to get it up and running. If a partner joins the business when such surplus is present, then it is only fair that Sash pays for that benefit. The accounting entries are:

Dr Partners’ capital account using new profit sharing ratio (PSR)

Cr Partners’ capital account using old profit sharing ratio (PSR).

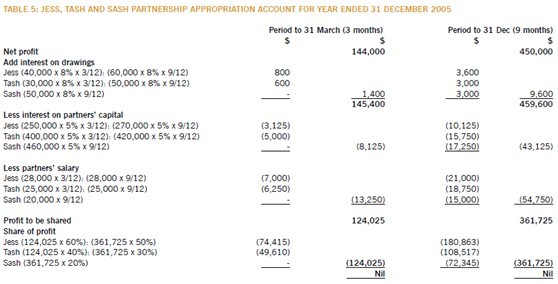

(b) Jess, Tash and Sash

Table 5 on page 65 shows the appropriation account for the year ended 31 December 2005.

Calculating the profit

In order to prepare the capital part of the balance sheet for a partnership, there are three workings that must be completed: partners’ appropriation account, partners’ current account, and partners’ capital account.

Page:1 2 See the original article>>

Copyright © 2000 - www.electedteal.com All Rights Reserved. 北京正保會計科技有限公司 版權所有

京B2-20200959 京ICP備20012371號-7 出版物經營許可證 ![]() 京公網安備 11010802044457號

京公網安備 11010802044457號

套餐D大額券

¥

去使用 主站蜘蛛池模板: 精品免费视频一区二区 | 野花成人免费视频 | 亚洲一区二区精品在线 | 国产三级电影在线播放 | 久久久久久一区二区三区四区别墅 | 国产精品久久一区二区三区动漫 | 欧美日韩国产精品 | 免费观看成人 | 久久久久久精 | 国产精品爱久久久久久久 | 99久久99九九99九九九 | 亚洲欧美日韩综合 | 免费的av | 99精品欧美一区二区三区 | 偷拍第一页| 日本特黄a级高清免费大片 韩国精品久久久 | 黄色片视频免费 | 久久久久久久 | 久久福利 | 久久国产精品二国产精品 | 亚洲欧洲日本在线 | 国产一区视频网站 | 爱情岛论坛亚洲线路一 | 久久久综合精品 | 精品久久久精品 | 91久久久久久久久久久 | 久久这里精品 | 精品嫩草| 99精品国产高清在线观看 | 久久久久国产精品一区 | 亚洲国产精品99久久久久久久久 | 国产精品久久久久久久久久免费 | 日韩一二区 | 日韩欧美专区 | 成人在线黄色电影 | 亚洲欧美视频在线观看 | 毛片国产 | 九九久久精品 | 成人在线视频一区 | 97国产在线观看 | 在线观看黄网 |

新用戶掃碼下載

新用戶掃碼下載