新用戶掃碼下載

新用戶掃碼下載

掃碼下載APP

及時接收考試資訊及

備考信息

This article looks at the various methods of re-apportioning service cost centre costs

When calculating unit costs under absorption costing principles each cost unit is charged with its direct costs and an appropriate share of the organisation’s total overheads (indirect costs). An appropriate share means an amount that reflects the time and effort that has gone into producing the cost unit.

Service cost centres are those that exist to provide services to other cost centres in the organisation. They do not work directly on producing the final product. Consequently, their costs must be re-apportioned to production cost centres so that their overheads can be absorbed into the final product. This article looks at the various methods of re-apportioning service cost centre costs.

THE DIRECT METHOD

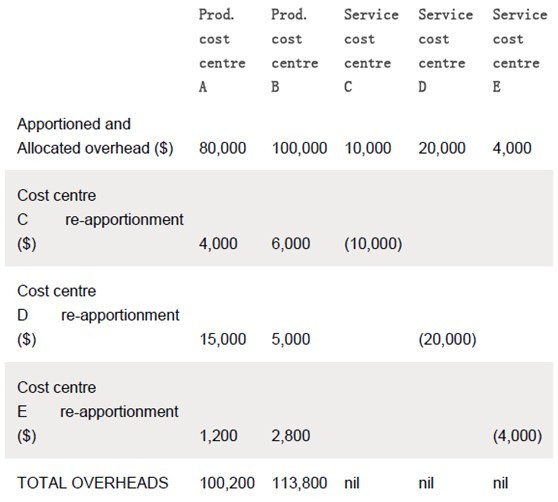

This is the simplest method and is ideal to use when service cost centres provide services to production cost centres, but not to each other. Example 1 considers such a situation.

Example 1

A company’s overheads have been allocated and apportioned to its four cost centres as shown below.

In this situation, service cost centre overheads are simply ‘shared out’ on the basis of usage. For example, production cost centre A should be charged with 40%, 75% and 30% respectively of cost centre C and D and E’s overhead costs. This would result in the following re-apportionment.

Tip: To check that you have not made any arithmetic errors, check that overhead ‘going in’ ($80,000 + $100,000+ $10,000 + $20,000 +$4,000 = $214,000) equals overhead ‘going out’ ($100,200 + $113,800 =$214,000)

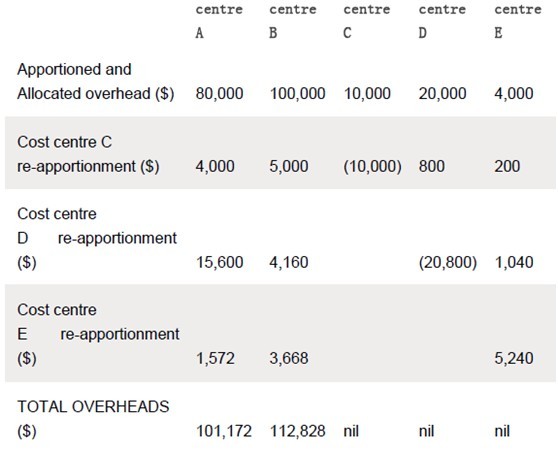

THE STEP DOWN METHOD

This approach is best used where some service cost centres provide services to other service cost centres, but these services are not reciprocated. Example 2 considers this situation. Cost centre C serves centres D and E, but D and E do not reciprocate by serving C. In these circumstances the costs of the service cost centre that serves most other service cost centres should be reapportioned first. We then ‘step down’ to the service cost centre that provides the second most service, and so on.

Example 2

Data as Example 1 apart from usage of C, D and E’s services has changed. Usage of service cost centres is as follows:

Copyright © 2000 - www.electedteal.com All Rights Reserved. 北京正保會計科技有限公司 版權所有

京B2-20200959 京ICP備20012371號-7 出版物經營許可證 ![]() 京公網安備 11010802044457號

京公網安備 11010802044457號

套餐D大額券

¥

去使用 主站蜘蛛池模板: 性爱免费视频 | 国产视频一区二区三区四区 | 国产一区二区三区精彩视频 | 亚洲精品午夜 | 日韩中文字幕av | 美女视频网站久久 | 国产精品久久久久久久久久免费 | 国内精品久久久久久影视8 成人午夜影院 | 国产黄a三级三级三级av在线看 | 成人黄色小视频 | 成人精品国产免费网站 | 久久xx | 精品久久网站 | 日韩欧美在线播放视频 | 精品久久99 | 亚洲iv一区二区三区 | 久久久午夜精品理论片中文字幕 | 精品综合网 | 精品一区二区国产 | 在线观看亚洲人 | 99在线精品视频 | 久久精品福利视频 | 91亚洲国产精品 | 精品无套 | 综合久 | 中文自拍 | 国产亚洲欧洲 | 亚洲精品大全 | 国产精品亚洲视频 | 婷婷丁香六月 | 亚洲一区在线观看视频 | 久久日本| 欧美福利在线观看 | 日韩三级一区 | 99热在线播放 | 18视频网站在线观看 | 国产成人在线播放 | 日韩精品视频免费观看 | 久久嫩草精品久久久精品才艺表演 | 亚洲成人av电影网站 | 日本久久久一区二区三区 |

新用戶掃碼下載

新用戶掃碼下載