掃碼下載APP

及時(shí)接收考試資訊及

備考信息

新用戶掃碼下載

新用戶掃碼下載安卓版本:8.7.95 蘋果版本:8.7.95

開發(fā)者:北京正保會(huì)計(jì)科技有限公司

應(yīng)用涉及權(quán)限:查看權(quán)限>

APP隱私政策:查看政策>

HD版本上線:點(diǎn)擊下載>

This article is relevant to candidates sitting Paper F6 (UK) in either June or December 2013, and is based on tax legislation as it applies to the tax year 2012–13 (Finance Act 2012).

Overseas aspects of corporation tax may be examined as part of Question 2, or it could be examined in Questions 4 or 5.

Company residence

Companies that are incorporated in the UK are resident in the UK. Companies that are incorporated overseas are only treated as being resident in the UK if their central management and control is exercised in the UK. Companies that are resident in the UK (or treated as being resident in the UK) are subject to UK corporation tax on their worldwide profits (including chargeable gains).

Example 1 Crash-Bash Ltd is incorporated overseas, although its directors are based in the UK and hold their board meetings in the UK.

· Companies that are incorporated overseas are only treated as being resident in the UK if their central management and control is exercised in the UK.

· Since the directors are UK based and hold their board meetings in the UK, this would indicate that Crash-Bash Ltd is managed and controlled from the UK, and therefore it is resident in the UK.

· If the directors were to be based overseas and to hold their board meetings overseas, the company would probably be treated as resident overseas since the central management and control would then be exercised outside the UK.

Overseas dividends

As far as Paper F6 (UK) is concerned all overseas dividends are exempt from UK corporation tax.

Exempt overseas dividends are included as franked investment income when calculating a company’s augmented profits in exactly the same way as UK dividends, unless they are group income. In this case they are completely ignored for tax purposes.

Example 2

During the year ended 31 March 2013 Various Ltd, a UK resident company, received an overseas dividend of £67,500 (net). Withholding tax was withheld from the dividend at the rate of 15%.

· If Various Ltd owns 50% or less of the voting power of the overseas company, then the overseas dividend will be exempt from UK corporation tax but included as

· If Various Ltd owns more than 50% of the voting power of the overseas company, then the dividend will be exempt from UK corporation tax and not included as franked investment income. This is because the overseas dividend is group income.

Overseas branches

An overseas branch of a UK company is effectively an extension of the UK trade, and 100% of the branch profits are assessed to UK corporation tax. Double taxation relief is then given where an overseas branch’s profits are also taxed overseas. Relief is restricted to the amount of UK tax on the overseas branch’s profits. If an overseas branch makes a trading loss then the loss can be relieved against UK profits.

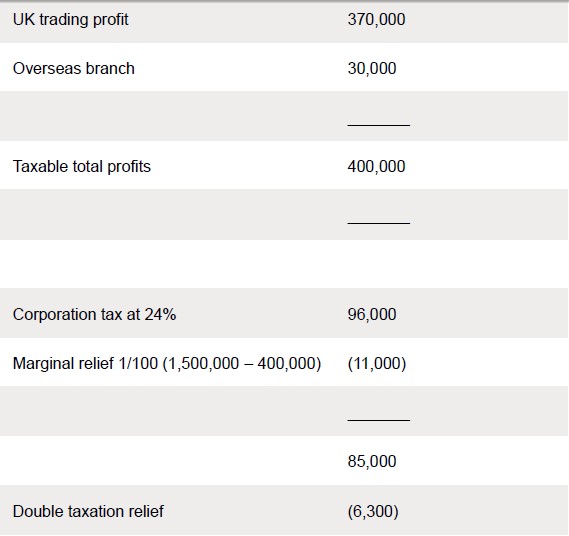

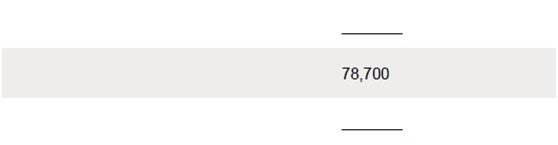

Example 3

Gong Ltd is a UK resident company with an overseas branch. For the year ended 31 March 2013 the company made a trading profit of £370,000, and the branch made a trading profit of £30,000. Overseas corporation tax of £6,300 was paid in respect of the overseas branch’s trading profit.

Gong Ltd’s corporation tax liability for the year ended 31 March 2013 is as follows:

The overseas branch has paid overseas corporation tax of £6,300, and this is lower than the related UK corporation tax of £6,375 (85,000 x 30,000/400,000).

As an alternative to this treatment it is possible for a company to elect to simply treat the profits of all of its overseas branches as being exempt from UK corporation tax. The election, once made, is irrevocable, and it applies to all of a company’s overseas branches. The election must be made before the start of an accounting period to which it is to apply.

An election will not be beneficial if a company has a loss making overseas branch, since if an election is made any trading loss of an overseas branch will not be relievable when calculating taxable total profits. Even if a branch is currently profitable, a company might decide not to make an election if double taxation relief means there is little or no UK corporation tax liability in respect of the branch profits. This will mean that relief will then be available should the branch make a loss at some point in the future.

See more>> See the original article>>

下一篇:考試規(guī)則

歷年樣卷

考試大綱

詞匯表

報(bào)考指南

考官文章

思維導(dǎo)圖

新用戶掃碼下載

新用戶掃碼下載安卓版本:8.7.95 蘋果版本:8.7.95

開發(fā)者:北京正保會(huì)計(jì)科技有限公司

應(yīng)用涉及權(quán)限:查看權(quán)限>

APP隱私政策:查看政策>

HD版本上線:點(diǎn)擊下載>

官方公眾號(hào)

微信掃一掃

官方視頻號(hào)

微信掃一掃

官方抖音號(hào)

抖音掃一掃

Copyright © 2000 - www.electedteal.com All Rights Reserved. 北京正保會(huì)計(jì)科技有限公司 版權(quán)所有

京B2-20200959 京ICP備20012371號(hào)-7 出版物經(jīng)營(yíng)許可證 ![]() 京公網(wǎng)安備 11010802044457號(hào)

京公網(wǎng)安備 11010802044457號(hào)

套餐D大額券

¥

去使用 主站蜘蛛池模板: 日韩欧美一区二区三区免费观看 | 久久精品国产一区二区三区 | 免费麻豆 | 日韩不卡免费视频 | 久久99网 | 中文字字幕一区二区三区四区五区 | 理论片在线看片三免费 | 91在线一区| 国产剧情一区二区三区 | 中文字幕av网站 | 亚洲高清在线视频 | 日韩高清免费观看 | 免费观看av网站 | 国产黄| 日韩欧美国产高清 | 99久久99久国产黄毛片 | 黄色一级视频免费看 | 亚洲一区久久 | 精品成人av一区二区在线播放 | 亚洲精选久久 | 欧洲一区二区在线 | 懂色av蜜臀av粉嫩av分享吧 | 国产片网站 | 精品66| 中文在线中文a | 久久精品免费 | 国产精品视频一区二区免费不卡 | 天天天天干 | 精品一区中文字幕 | 久久久一二三 | 三级电影免费观看 | 高清国产一区二区三区四区五区 | 亚洲精品久久久久中文字幕欢迎你 | 久久九九国产 | 成人毛片网站 | 欧美激情视频一区二区三区 | 国产一区中文字幕 | 超黄网站 | 亚洲福利视频一区 | 日韩经典一区二区 | 婷婷人人爽人人 |